#Mr. Rohan Byanjankar

#E-mail : rohanbjkr@gmail.com

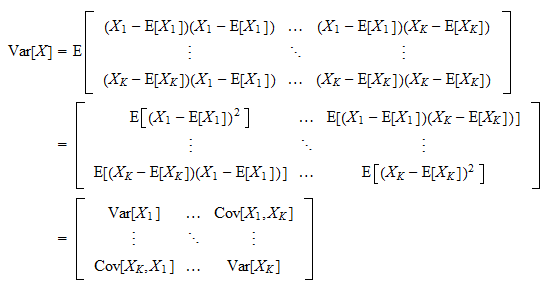

#Manual Calculation of Variance Covariance Matrix in R

# This dataset has been Taken from "An Introduction to Econometrics by Christopher Dougherty"

#Data file saved in Siddha Sir's Blog

datafile<- read.csv("https://sites.google.com/site/siddhabhatta/data/data3.csv", header=T)

#Derivation of Variance Covariance Matrix

#Formula: [X - [1 1'X]/n]'*[X - [1 1'X]/n]

attach(datafile)

y = wage_rate

X = cbind (yearsedu, exp, ASVABC)#Extract yearsedu, exp and ASVABC from datafile

X1 <- matrix(1:1, nrow=540, byrow=TRUE)#Matrix of 540x1 with "1"

X1t <- t(X1)#transpose of X1

n <- nrow(X1)

varcov1 <- ((t(X-(X1%*%((X1t%*%X)/n))))%*%(X-(X1%*%((X1t%*%X)/n))))/n

varcov1

Result

yearsedu exp ASVABC

yearsedu 5.935154 -2.351877 13.532991

exp -2.351877 19.612091 2.532059

ASVABC 13.532991 2.532059 91.385882

Post a Comment